Millennials and Gen Z Are Redefining Debt Collection Expectations

By Adam Parks

Millennials and Gen Z are changing the rules for debt collection. These digital-native generations have grown up with smartphones, on-demand apps, and real-time communication. They expect every financial interaction to match that standard.

For traditional debt collectors, this creates a critical change. Old strategies that rely heavily on outbound phone calls, mailed notices, and rigid scripts are no longer effective. The expectations of modern consumers require a more flexible, personalized, and tech-savvy approach.

A recent survey shows that 70% of Millennials and 63% of Gen Z want mobile-first, embedded financial services. These consumers are not just open to digital solutions, they actively seek them out and judge brands based on how well they deliver. Their adoption of fintech is significantly higher than that of older generations, and that includes the way they expect debts to be managed and resolved.

Understanding Millennial and Gen Z Debt Profiles and Payment Behavior

While younger consumers embrace digital experiences, many also carry significant financial burdens. The average Millennial holds around $94,000 in personal debt, and over 60% of Gen Z borrowers have already experienced at least one account delinquency. Much of this debt is tied these generations. BNPL services, which are particularly popular among Gen Z, are designed to be quick, seamless, and interest-free if paid on time. Over 50% of Gen Z consumers have used BNPL in the last year. These platforms create a very different user expectation, one that favors ease, flexibility, and transparency.

Why Phone Calls and Mail Fail with Modern Fintech Borrowers

One of the most significant mismatches between traditional collectors and fintech consumers lies in communication.

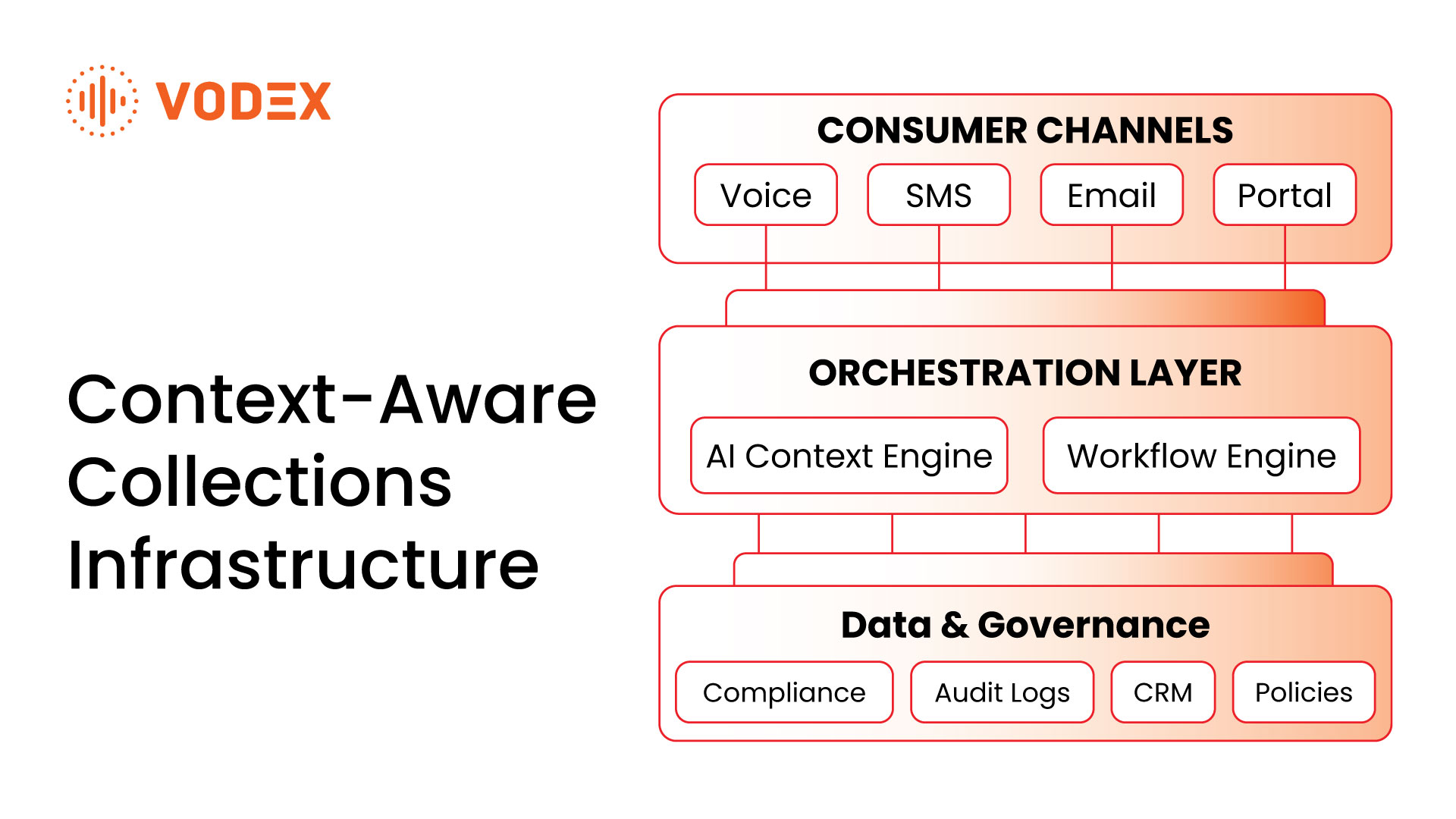

Gen Z and Millennials overwhelmingly prefer text, email, and in-app messaging over phone calls. Researchers found that Gen Z expects always-on communication with companies, including 24/7 chat availability and real-time updates. These consumers also gravitate toward platforms that allow them to engage on their own terms, rather than being pressured into conversations through unsolicited phone calls. The increased use of call blockers like RoboKiller and the native additional of call screening on both Android and iPhones will exacerbate the challenges in 2025 and beyond.

Rick Winters, Chief Operating Officer at National Credit Adjusters, has seen this evolution firsthand.

“The ultimate goal is to have as many communication channels as possible available, and then figure out what the optimal channels are for each individual consumer,” he said. “Through the last how many years, we’ve evolved, and we are now leveraging more than the traditional phone.”

This shift is not merely about convenience. It reflects a broader desire for autonomy and respect in the debt resolution process. When consumers feel they can control how and when they interact with a collector, they are more likely to engage constructively.

The Role of Transparency and Self-Service in Digital Debt Collection

Fintech borrowers expect real-time access to information about their accounts. This includes current balances, due dates, interest accrual, and payment options. Legacy collection practices often rely on opaque processes, where consumers must speak with a representative to understand their situation. That approach creates unnecessary friction and erodes trust.

Self-service portals provide a meaningful solution. When borrowers can explore repayment plans, make payments, or ask questions through a secure and intuitive interface, it increases both satisfaction and performance. According to data from Quiq, companies that implement automated self-service options see an engagement rate of up to 80%, significantly outperforming the 20 to 30% engagement rates of phone-based strategies.

Transparency is also about tone. Consumers are more responsive to messages that provide clear, respectful explanations rather than pressure or legal threats. Debt recovery must align with the same design and tone principles these generations experience from every other digital service.

How Personalization Improves Debt Recovery for Younger Generations

Younger borrowers have grown accustomed to tailored experiences. Platforms like Spotify, Netflix, and Amazon constantly adapt to user behavior. This personalization creates a standard that extends to financial services as well. In debt collection, that means going beyond batch-and-blast outreach.

Behavioral analytics can help identify the best time to reach each consumer, what tone to use, and which repayment options are most likely to succeed. Personalization also requires consent and sensitivity. Gen Z in particular is wary of companies that overreach or mismanage their data.

The goal is to build systems that recognize individual preferences without becoming invasive. Younger adults respond better when they feel the approach is appropriate to their context, rather than rigid or formulaic. Collectors who understand and apply these insights can significantly improve repayment outcomes.

Digital Collection Strategies That Engage Fintech-Savvy Consumers

Modernizing collection practices for fintech consumers requires investment, but the payoff is substantial. Digitally optimized outreach not only improves engagement but reduces costs and boosts brand credibility.

The most successful strategies will be those that:

- Offer intuitive, mobile-first portals for account management

- Use AI chatbots and messaging to enable 24/7 communication

- Tailor messages based on communication preferences and behavioral signals

- Provide transparent, flexible repayment plans modeled after familiar digital products like BNPL

As Rick Winters added: “I’m really excited about this evolution. We are using analytics to personalize contact strategies in ways that actually help consumers. It’s better for everyone.”

Adapting Debt Collection for the Fintech Generation

The expectations of Millennial and Gen Z borrowers are clear. They want debt collection that mirrors the rest of their digital lives. Traditional approaches that focus on outbound dialing and mailed letters are increasingly ineffective with this population.

To remain relevant, the collections industry must evolve into a digital-first, consumer-centric service. This means building infrastructure that allows borrowers to resolve debts on their terms, while maintaining compliance and delivering strong recovery results. Forward-looking organizations are already moving in this direction, and those who delay may find themselves out of step with the largest group of borrowers in the financial ecosystem.

If you’re interested in exploring how your collection strategy can adapt to meet the needs of fintech consumers, now is the time to start the conversation.to fintech-originated products like personal loans, BNPL (Buy Now, Pay Later) services, and unsecured credit lines.

Although the debt load is high, it is the type of debt and how it was incurred that differentiates