Evaluating Digital Consumer Journeys: Rethinking Authentication and Self-Service in Collections

Abstract

Evaluating digital consumer journeys is about far more than user experience design. In this article, I share why reducing authentication friction, expanding self-service beyond payments, and tracking failure events are essential strategies for debt collection agencies aiming to build trust and drive payment outcomes.

Introduction

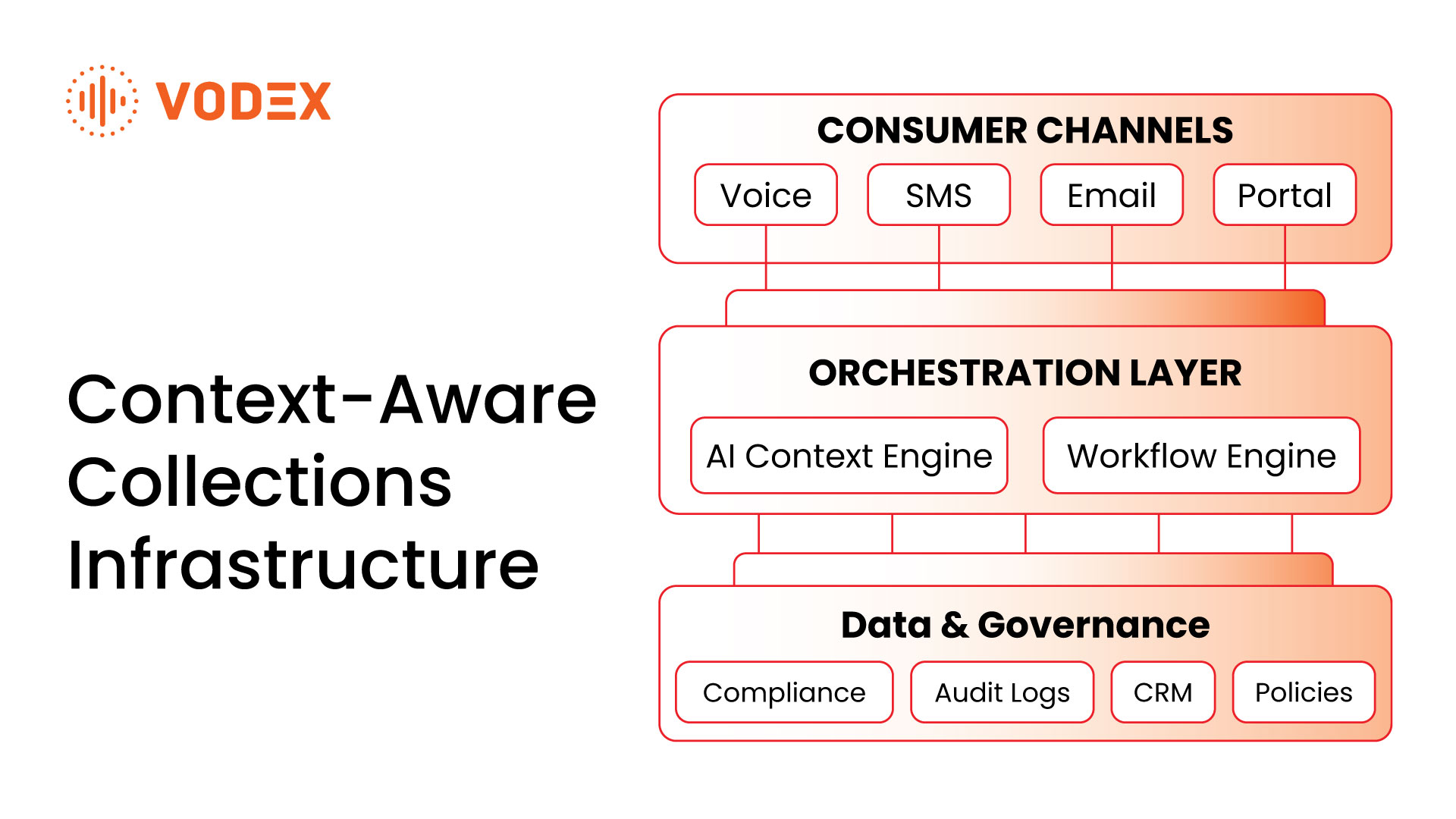

In the current debt collection landscape, digital transformation has become a foundational priority. Yet despite broad investments in portals, payment systems, and communication tools, many agencies continue to struggle with low conversion rates and consumer engagement. From my experience leading Concepts2Code, I’ve seen that evaluating digital consumer journeys holistically – from authentication to data tracking – is the missing link.

Too often, agencies focus on their outreach strategies without evaluating the end-to-end consumer experience. When authentication friction, portal limitations, or data blind spots persist, outreach effectiveness declines, and consumers are left frustrated rather than empowered.

Reducing Authentication Friction

Most agencies implement authentication strategies that prioritize compliance over practicality. While compliance is non-negotiable, so is consumer usability.

I frequently encounter portals requiring consumers to enter obscure account numbers they rarely know. In my view, this single requirement alone can reduce successful logins by more than half. Consumers remember their phone number, email, and basic personal identifiers. Designing authentication flows using accessible identifiers reduces friction and improves payment conversions.

I believe agencies should also consider allowing one-time payments with limited authentication when necessary. While some argue this increases risk, refusing payments altogether due to verification issues is a guaranteed revenue loss. Ultimately, it’s about balancing compliance with operational strategy.

Designing Self-Service Portals Beyond Payments

Portals in collections have historically been designed as digital cash registers. This mindset limits their potential impact.

Consumers don’t just want to pay; they want to manage their obligations. Effective portals provide options to:

- Update contact information

- Submit disputes or complaints

- Upload bankruptcy notices or attorney representation forms

- Adjust communication preferences

When consumers gain control, agencies build trust. And trust translates into higher resolution rates, fewer escalated complaints, and improved brand reputation. In my work with agencies, the highest-performing portals are built as self-service hubs rather than narrow payment gateways.

Tracking Failures as Operational Insights

Many agencies track successful payments but ignore failed logins, abandoned carts, or payment declines.

This is a missed opportunity. Failure events are not dead ends; they are signals of consumer intent blocked by friction.

For example, tracking failed login attempts enables targeted outreach to consumers who attempted to resolve but couldn’t complete authentication. Monitoring payment declines or NSFs can inform better communication timing and follow-up strategies.

Operational visibility into these failure events transforms agency performance from reactive to proactive. In my experience, agencies that integrate failure tracking into their CRM workflows consistently outperform those that rely only on success metrics.

Leveraging API Integrations for Real-Time Data Flow

API integrations remain underutilized in collections technology stacks. They are often perceived as complex or unnecessary, but APIs provide:

- Real-time data synchronization

- Reduced risk by avoiding duplicate databases

- Flexibility to integrate with evolving AI and analytics tools

I describe APIs as the invisible infrastructure that connects systems securely in real time. For example, when a consumer updates their phone number in a portal, an API ensures that the change is reflected immediately in the agency’s CRM without manual re-entry.

API-enabled architectures not only improve operational efficiency but also enhance consumer trust by ensuring accurate data across touchpoints.

Integrating Failure Analytics with Operational Strategy

According to TransUnion’s 2024 Debt Collection Industry Report, 88% of agencies now utilize self-service portals. However, few analyze consumer journey data beyond aggregate payment success rates.

I believe agencies must implement journey analytics that measure:

- Authentication drop-offs

- Form field abandonment rates

- Mobile versus desktop completion rates

With this data, operational leaders can refine portal design, adjust communication scripts, and prioritize technology enhancements that directly impact payment outcomes.

Conclusion

Evaluating digital consumer journeys is no longer optional for agencies aiming to remain competitive. Authentication friction, limited self-service design, and failure data blind spots silently undermine revenue and consumer trust every day.

As agencies plan their next technology investments, I urge leaders to view portals not simply as compliance tools or payment systems but as strategic assets. When designed and evaluated holistically, portals become trust-building, revenue-generating solutions that align with modern consumer expectations.

It’s time to rethink how we define a successful digital consumer journey.

Author Bio

I’m Mark Reinhard, CEO of Concepts2Code, where we build flexible self-service portals, payment solutions, and digital communications tailored for debt collection agencies and financial services firms. My focus is on designing digital solutions that balance compliance, operational efficiency, and consumer experience.