A Use Case–Driven Approach to AI Adoption in Debt Collection

Artificial intelligence is now a permanent component of debt collection operations. While early adoption focused on experimentation and proof-of-concept initiatives, the industry has entered a phase where AI must be evaluated as operational infrastructure rather than emerging technology.

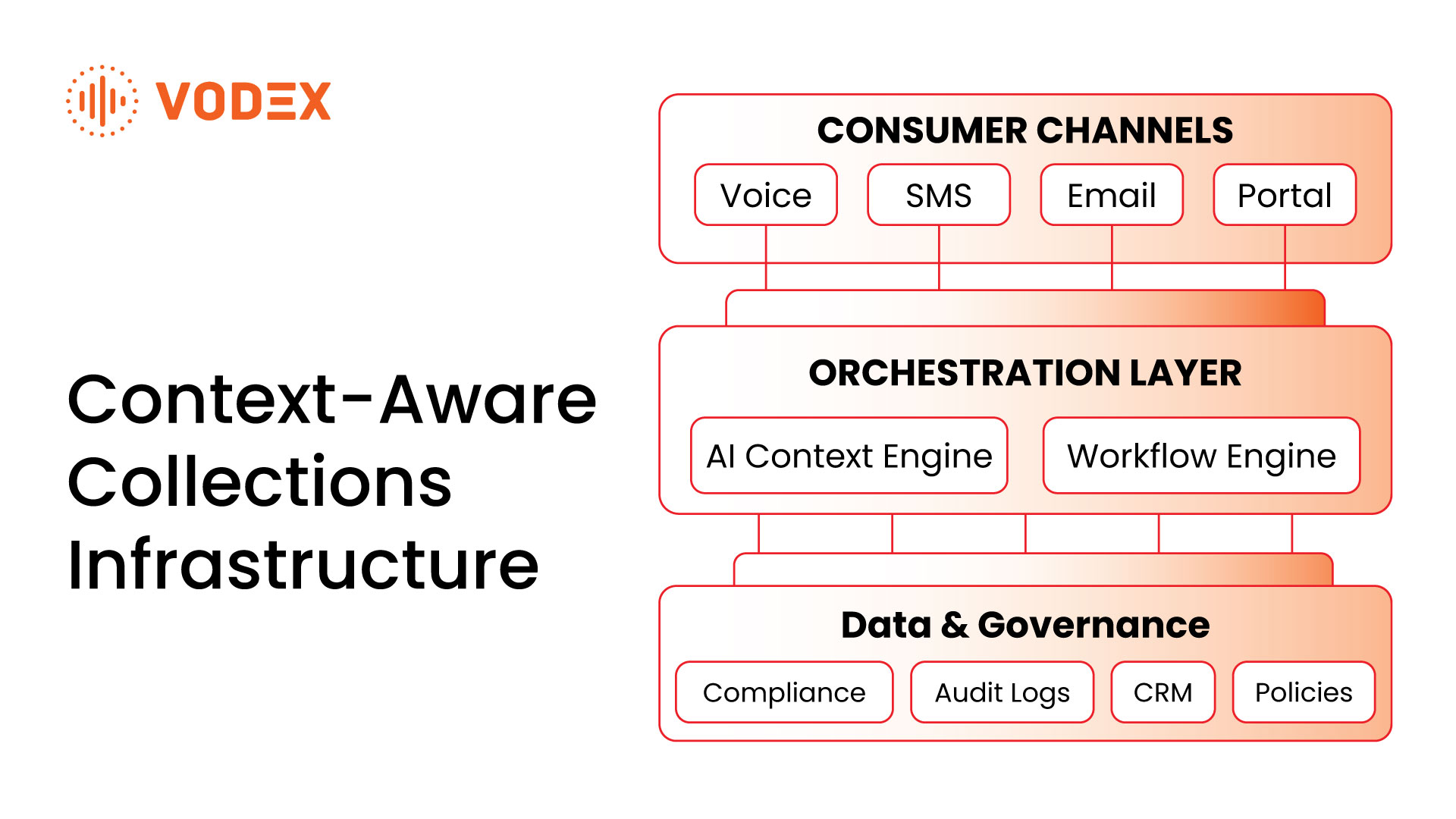

From a systems perspective, successful AI adoption in the debt collection industry depends on clearly defined use cases, governance structures, and an understanding of where automation enhances outcomes versus where human oversight remains essential. Without this discipline, AI increases operational risk rather than reducing cost or improving performance.

This article presents a structured analysis of AI use cases in debt collection operations, emphasizing governance-first deployment and the conditions under which AI can scale operational efficiency without increasing headcount.

The Shift From AI Experimentation to Operational Design

Early AI adoption in collections was characterized by fragmented pilots, vendor-led demonstrations, and isolated automation projects. These efforts often produced localized gains but failed to deliver durable, enterprise-wide value.

As regulatory scrutiny and portfolio complexity increased, it became evident that AI must be deployed within a defined operational architecture. Use cases now precede tools. Decision ownership, auditability, and escalation paths must be established before AI systems are integrated into live workflows.

This transition marks a critical maturation point in AI adoption in the debt collection industry.

A Structured Breakdown of AI Use Cases in Debt Collection Operations

Despite the growing number of AI vendors and technologies entering the market, the functional application of AI in collections is relatively consistent. Most deployments fall into a limited set of operational categories. Understanding these categories allows executives to assess value, risk, and governance requirements more effectively.

Quality and Compliance Monitoring

AI is increasingly used to analyze large volumes of recorded calls, written communications, and digital interactions. Rather than replacing compliance teams, these systems enable exception-based review models, allowing human resources to focus on high-risk interactions.

This use case is foundational because it improves coverage and consistency while maintaining regulatory defensibility.

Chat and Written Communication Support

AI-driven chat and messaging systems support consumer communications by improving responsiveness and standardization. In regulated collections, these tools function most effectively when governed as assistive technologies rather than autonomous decision-makers.

Governance controls determine message templates, escalation triggers, and audit trails, ensuring compliance obligations are met.

Scoring and Treatment Strategy Optimization

Analytical AI models are widely applied to scoring, segmentation, and treatment path design. These use cases focus on decision intelligence rather than consumer interaction, making them lower risk and highly scalable.

Organizations frequently develop or customize these models internally due to their direct impact on pricing, liquidation forecasting, and competitive differentiation.

Voice AI and Agent Assist

Voice-based AI has attracted significant attention, but risk profiles vary substantially. Agent assist technologies enhance live conversations by providing prompts, compliance guidance, and real-time insights while preserving human accountability.

Fully autonomous voice systems, by contrast, introduce material governance challenges related to latency, accuracy, escalation, and explainability. Adoption in this area remains cautious and uneven.

Negotiation Support and Offer Modeling

AI-driven negotiation tools analyze historical outcomes to inform settlement strategies and payment options. These systems support consistency and optimization but do not replace human judgment in regulated interactions.

Their value lies in improving decision quality rather than automating outcomes.

Operational Analytics and Risk Forecasting

Operational analytics represents one of the most durable AI use cases in debt collection operations. By identifying trends, forecasting performance, and highlighting emerging risks, these tools support executive decision-making and long-term planning.

This category often delivers value without introducing consumer-facing risk.

AI Governance in Regulated Collections

Across all use cases, governance is the determining factor of success. AI governance in regulated collections establishes decision authority, defines escalation paths, and ensures that AI outputs are interpretable and auditable.

Without governance, AI systems amplify inconsistency. With governance, they reinforce operational discipline.

Effective governance frameworks clarify which AI outputs are advisory, which are executable, and which require human approval. This structure is essential for regulatory defensibility and organizational trust.

Scaling Operational Efficiency Without Headcount Growth

A common misconception is that AI adoption primarily serves workforce reduction. In practice, the most successful deployments focus on capacity redesign rather than labor replacement. For me, this is the single most important facet of AI providing value to the enterprise, and is often the most misunderstood.

By automating low-judgment tasks and accelerating exception identification, AI allows organizations to scale collections performance without headcount growth. Human expertise is redirected toward oversight, negotiation, and higher value activities.

Operational efficiency strategy for collections increasingly depends on this reallocation of effort rather than cost elimination. After all, we all look at what we wanted to accomplish and compare it to what we actually accomplished at the end of the month. How often are you disappointed? AI helps me meet my lofty goals.

Evaluating AI Risk in Consumer Communications

Consumer-facing AI introduces heightened regulatory exposure. Evaluating AI risk in consumer communications requires scrutiny of system latency, error tolerance, escalation logic, and data governance.

Agent-assisted models offer a lower-risk entry point by maintaining human oversight. Autonomous systems demand higher levels of technical maturity and governance rigor, which many organizations are still developing.

Risk evaluation should be use case–specific rather than technology-driven.

Build Versus Buy Considerations

Not all AI capabilities warrant external procurement, nor should all systems be developed internally. Build-versus-buy decisions depend on strategic differentiation, resource availability, and governance capacity. Right now, in this market, I’m a buyer not a builder.

Analytical models tied to proprietary strategies often favor internal development. Real-time AI systems typically require external platforms due to infrastructure and compute requirements.

Clear alignment between use case and sourcing strategy is essential for sustainable AI adoption.

Conclusion

AI adoption in the debt collection industry is no longer defined by novelty. It is defined by governance, clarity of use case, and operational integration.

Organizations that succeed will treat AI as infrastructure rather than experimentation. By grounding adoption decisions in a structured use case framework, leaders can scale operational efficiency while maintaining regulatory integrity.

The future of AI in collections belongs to disciplined operators, not just early adopters alone.