Solo’s Evolution and Its Implications for Receivables Operations

The U.S. receivables industry continues to operate on infrastructure and behavioral assumptions developed decades ago. Many of these no longer align with current consumer expectations or operational realities. Call-center-driven outreach, negotiation sequences based on limited information, and manual task cycles place enormous pressure on both collectors and consumers. As a result, resolution timelines lengthen, compliance risk increases, and large portions of portfolios remain unrecovered.

The evolution of the Solo platform emerged from recognizing these systemic limitations and rethinking debt resolution from the ground up. The underlying premise is straightforward: resolution is more efficient and predictable when both parties operate with accurate information, automation supports workflow consistency, and digital pathways replace friction-heavy engagement.

This article outlines the strategy, data principles, and modernization frameworks driving Solo’s development and the broader transformation now reshaping debt resolution technology.

Rethinking Traditional Collection Workflows Through High-Information Models

The debt resolution process has historically relied on low-context interactions. Collectors must assess ability-to-pay without reliable data, while consumers often lack clarity on their financial options. This information asymmetry results in stalled negotiations, fear-driven responses, and low settlement accuracy.

A high-information model solves this problem. Verified financial data assessment such as income verification, spending trends, and cash-flow analysis, provides a factual foundation for mutually sustainable solutions. When settlement parameters align with a consumer’s actual financial profile, negotiation shifts from positional bargaining to objective decision-making.

This shift enables three measurable improvements:

- Higher Settlement Accuracy

Terms align more closely with financial reality, reducing broken promises and re-default. - Reduced Negotiation Friction

Fewer back-and-forth exchanges are required because feasibility is established upfront. - Increased Consumer Trust

Consumers engage more readily when transparency replaces uncertainty.

The evolution of the Solo platform is built on this high-information foundation, integrating verified data directly into the resolution workflow.

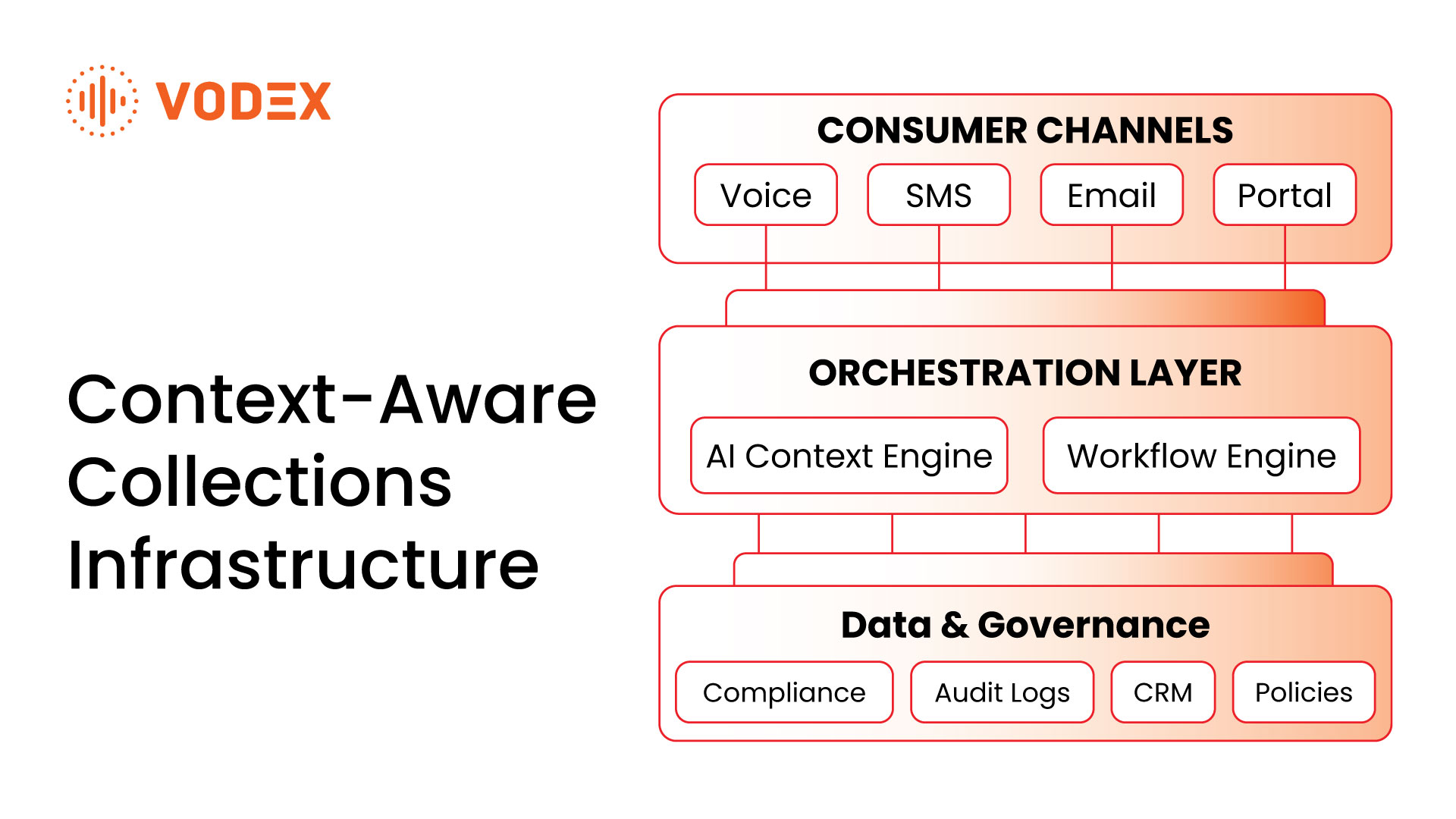

Closing Operational Gaps With Next-Generation Debt Resolution Tools

Traditional collection operations lean heavily on manual execution: generating disclosures, confirming terms, issuing letters, and re-verifying consumer details. These tasks are essential for compliance but consume a disproportionate amount of collector time.

Next-generation debt resolution tools address these inefficiencies by embedding:

- automated disclosures

- instant settlement documentation

- real-time collectability scoring

- structured payment plan modeling

- compliant communication sequencing

- unified dashboards integrating all account insights

These enhancements do not replace human judgment. Instead, they elevate it by positioning collectors to focus on conversations requiring nuance while automation manages the administrative load.

Solo’s evolution therefore centers on translating high-information insights into actionable workflows, enabling collectors to resolve accounts in seconds, not minutes.

Understanding Consumer Behavior Through Accurate Financial Context

A persistent industry challenge lies in misunderstanding consumer intent. Approximately 70% of debt remains uncollected, not solely due to unwillingness to pay, but due to confusion, fear, or lack of clarity around available options.

Modernization requires addressing the behavioral context driving repayment outcomes:

- Consumers avoid engagement when they don’t understand what’s expected.

- They participate more when offered clear paths tailored to their capacity.

- They respond better to digital channels than traditional outreach.

Accurate financial context reduces the psychological barrier to engagement. When consumers see settlement terms grounded in their actual financial patterns, the process feels credible rather than adversarial.

The evolution of Solo emphasizes consumer clarity, financial transparency, and structured guidance. These elements directly improve conversion and liquidation performance.

Modernizing Debt Negotiation and Settlement Workflows

Modernization is not an abstract concept; it involves redesigning resolution pathways to remove friction at every stage. Key elements include:

1. Automated Workflow Components

Automation ensures consistent compliance execution, reduces errors, and accelerates settlement timelines.

2. Data-Driven Offer Structuring

Settlement brackets determined by verified insight eliminate unworkable agreements.

3. Digital-First Engagement

Mobile-friendly workflows support the real behavior patterns of today’s consumers.

4. Real-Time Feasibility Checking

Proposed terms are validated instantly, improving both sustainability and collector efficiency.

The modernization of debt negotiation and settlement workflows is essential for organizations seeking predictable performance in a digital environment.

Strengthening Financial Stability Through High-Trust Engagement

An overlooked dimension of debt resolution is its broader economic impact. When consumers resolve their obligations in manageable, data-informed structures, they reenter financial stability more quickly. Increased net worth is correlated with improved access to banking products, reduced risk, and stronger participation in the credit ecosystem.

High-trust, high-information tools contribute to this stability by:

- reducing default judgments

- minimizing long-term financial harm

- supporting more sustainable repayment behavior

- enabling consumers to transition out of avoidance cycles

The evolution of the Solo platform therefore supports not only operational efficiency for collectors but long-term financial health for consumers.

CONCLUSION

The evolution of the Solo platform represents a shift in how the industry approaches debt resolution: from intuition-driven to information-driven, from manual workflows to automation-supported systems, and from friction-heavy negotiation to transparent digital engagement.

Organizations that adopt high-information, high-trust tools will be positioned to improve liquidation performance, reduce operational cost, and enhance consumer experience. The future belongs to systems that prioritize clarity, data integrity, and workflow modernization.

The question for industry leaders now is not whether modernization is necessary, but which components of the resolution process must evolve first to remain competitive and compliant.

AUTHOR BIO

George Simons is the Co-Founder & CEO of Solo, a platform he built after experiencing firsthand how inaccessible debt defense can be for consumers. With a JD/MBA from BYU and leadership experience in legal-tech innovation, George brings a data-driven, human-centered perspective to the modernization of debt resolution.